After the Spiller Scandal, It Sure Looks Like the NJEA Is Losing Members: New Leadership Acts to Boost Membership

June 12, 2026Sunlight has embarked on a campaign to inform the half of teachers hired since 2011 about their worst-in-the-nation Tier 5 pension plan. As we have documented extensively, NJEA leadership wasted $45 million of teachers’ dues — as well as the resources and focus of the organization — on former-President Sean Spiller’s vanity run for governor and then dropped the ball on improving the lousy Tier 5 pensions. Over half of all teachers are now stuck with underfunded, inferior Tier 5 pensions, which stand in marked contrast with NJEA execs’ gold-plated, over-funded pensions. Would NJEA leadership have prioritized pensions if they had Tier 5 pensions rather than gold-plated ones?

NJEA leadership’s pensions are over-funded while teachers’ pensions are underfunded. Fortified with hundreds of millions of dollars of teachers’ highest-in-the-nation dues, NJEA leadership has ensured that their own pensions are very, very secure. How secure? The NJEA just filed its most recent US Department of Labor Form 5500 for NJEA leadership’s pension plan (the “Leadership Plan”). As of last year, the Leadership Plan was 111% funded (meaning that there is $1.11 set aside for each $1 owed), as compared to the Teachers Pension & Annuity Fund’s (TPAF) 61% (according the most recent actuarial report).** Leadership’s Plan is over-funded and the teachers’ plan is underfunded.

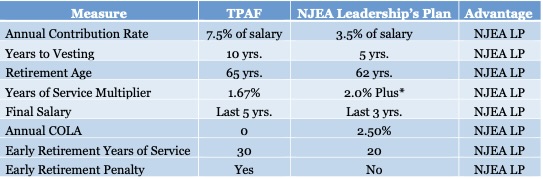

Leadership’s gold-plated pensions are also vastly superior. Not only are the NJEA leadership’s pensions much more secure, they are also vastly superior to teachers’ pensions. The table below provides a comparison between the current Tier 5 plan and the Leadership Plan.

Annual contribution rate: Teachers must contribute 7.5% of their annual salaries to their pensions compared to only 3.5% for leadership. Thus, a teacher with a $80,000 salary is forced to contribute $6,000 annually into TPAF — or $3,200 more per year than would a comparable NJEA employee — for a greatly inferior pension plan.

Years to vesting: Under TPAF’s formula, teachers must complete 10 years of service before they qualify for their pension while leadership needs only 5 years of service. The 10-year vesting requirement results in 45% of teachers not vesting at all, which can cost teachers thousands of dollars.

Retirement Age: TPAF’s normal retirement age for teachers hired is 65 years. The Leadership Plan’s retirement age is 62.

Final Salary: TPAF’s Final Salary is based on the average of a teacher’s salaries over the last five years of service versus the Leadership’s Plan’s last three years. For teachers, whose salaries automatically step up every year and who earn their highest salaries in their last years of service, it is disadvantageous to use the average of the final five years.

Years of Service (YOS) Multiplier: Both pension plans rely on a formula: YOS Multiplier x YOS x Final Salary. For TPAF, the retirement multiplier is 1.67 percent (1/60). The Leadership Plan has a retirement multiplier of 2.0 percent (1/50) plus an additional three supplements of 1/2 to 2/3 of a percent depending on YOS.

COLA: Very importantly, the Leadership Plan provides a 2.5 percent annual cost-of-living adjustment (COLA), which means that the retiree’s annual pension benefit compounds annually at 2.5 percent for every year of retirement. Over a 25-year retirement, the COLA makes an enormous difference in total pension benefits paid out (cumulatively, it amounts to an 85% increase in benefits). The longer the retirement, the greater the impact of the COLA.

Early Retirement: Under TPAF, a teacher with a minimum of 30 years of service may retire early, but if younger than 65 years, the teacher’s pension benefit will be reduced by 3% for every year that the retirement date precedes 65. So for a teacher with 30 years of service who chooses to retire at 55, the annual pension benefit would be reduced by 30 percent. Under the Leadership Plan, an employee with 20 years’ service can retire early upon reaching the age of 55 without a penalty. So a 20-year NJEA employee could choose to retire at 55, not 62, and still receive a full pension. So NJEA leadership have a real choice about retiring early after only 20 years of service. The teacher must work 30 years and then pay a substantial penalty, which is not much of a choice at all.

What if NJEA execs had Tier 5 pensions? We wonder if NJEA Leadership would have prioritized improving pensions if they, too, were stuck with inferior, underfunded Tier 5 pensions. What if the $45 million of dues wasted on Spiller had been devoted to a full, multi-year campaign for pension improvements? What if teachers had been given the opportunity to organize and mobilize to fight for their own pensions? What might have been achieved by a fully resourced campaign before Gov. Murphy left office?

We will never know. The facts are that leadership has very secure, gold-plated pensions and they dropped the ball on teachers’ pensions. NJEA leadership wins, teachers lose.

*Additional payments for length of service. See “Years of Service Multiplier” section. **This includes the 77.8% of lottery proceeds that have been dedicated to shoring up TPAF, without which TPAF would be a mere 50%-funded.