More Mendacity from Mendacious Michael Gottesman: Spewing Falsehoods About the New Jersey Family Policy Center

April 8, 2026Below-Trend NJ Corporate Tax Collections Coincide with Gov. Murphy’s Corporate Tax Hike

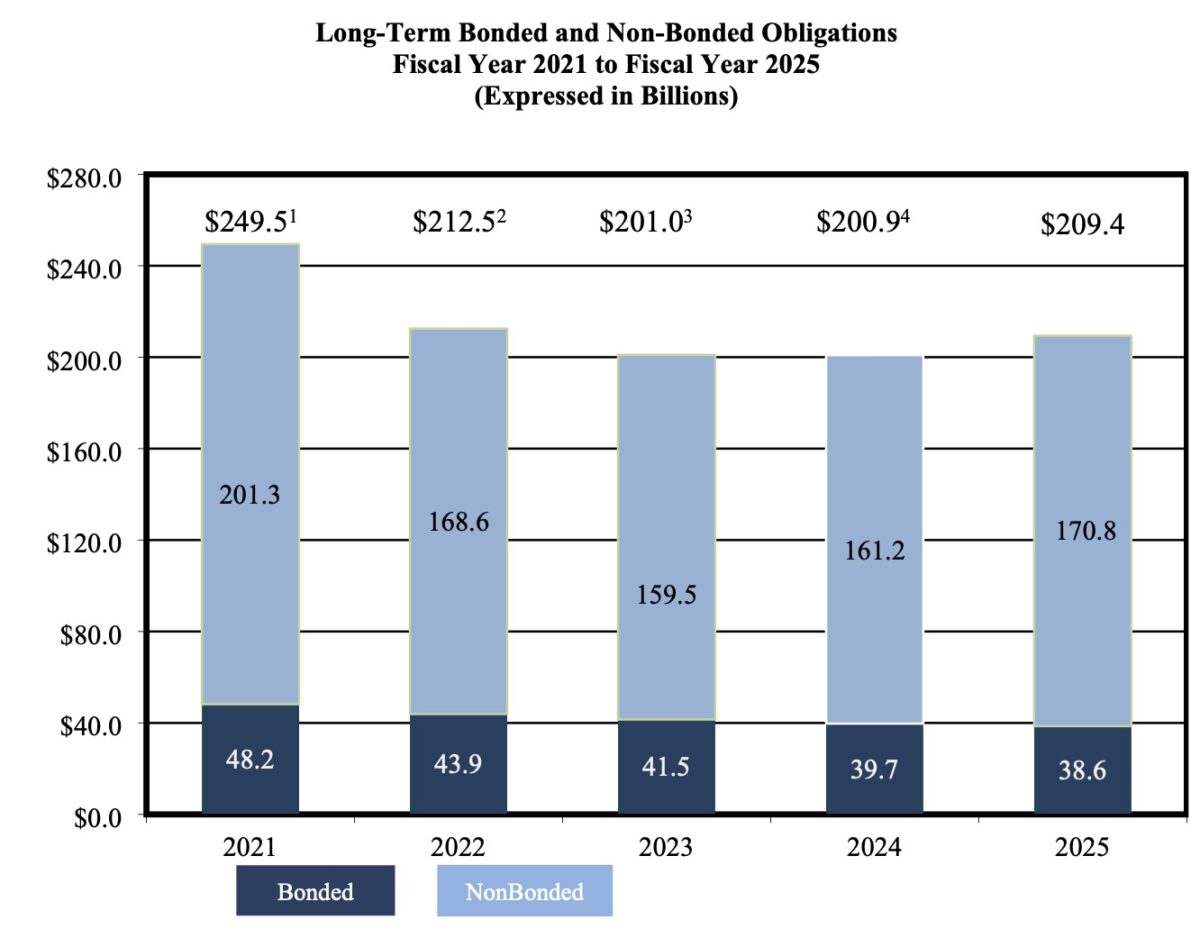

May 1, 2026In more excellent reporting, NJSpotlight News‘ John Reitmeyer presents the reality of New Jersey’s long-term debt profile, as shown in the state’s most recent, FY2025 (7/1/24 – 6/30/25) Annual Report. Former-Gov. Murphy chose to pump $47 billion into New Jersey’s pension system, but pensions make up only part of New Jersey long-term debt: there’s also bonded debt (bonds that the state issues) and state health benefits, which along with pensions make up the non-bonded debt. All of these — not just pensions — are funded by tax (and lottery) revenues, so while bonds have been paid own and pensions are on firmer (but still not firm) ground, the state’s health-benefit liabilities have dramatically increased. As a result, New Jersey’s total debt has essentially flat-lined since FY2022, when Murphy began making the full, required pension payments. And even pensions still face a significant funding challenge and will require three decades of $7 billion payments (over $200 billion in total) to be fully funded. It’s not a sustainable system.

Long-term debt decreased dramatically from FY2021 to FY2022. As can be seen in the graph below, New Jersey’s total debt level decreased from $250 billion during the COVID year of FY2021 to $213 billion in FY2022. Federal COVID aid and record tax revenues helped the state pay down bonded debt, but the drop in non-bonded debt was largely due to Murphy’s making the first full, required pension payment in FY2022. This led to revised actuarial assumptions* which caused the state’s non-bonded debt to drop from $201 billion in the FY2021 to $169 billion in FY2022.

Since FY2022, total long-term debt has flatlined. But what really stands out in the above graph is that since FY2022, New Jersey’s total long-term debt has flatlined, decreasing from $213 billion in FY2022 to $209 billion in FY2025, a mere 1.9%. As Reitmeyer points out, this is due to the substantial increase in non-bonded liabilities from FY2024 to FY2025.. That was entirely caused by a $12 billion increase in the state’s health-benefits liability.

Murphy’s $47 billion has not solved New Jersey’s debt problem. This underscores the limited effect of the $47 billion that Murphy pumped into the state pension system. New Jersey’s long-term debt is made up of bonds and unfunded pension and health-benefit liabilities. Bonded debt is down smartly and the state pension fund is now being fully funded, but state health benefits are funded on a pay-as-you-go basis from each year’s annual budget. New Jersey taxpayers are on the hook for ALL of this debt, regardless how it is categorized. Money is fungible. If $47 billion of tax (and all the lottery) revenues are being diverted to the pension fund and paying down bonds, then that is money that cannot be used to pay for increased health benefits.

Even pensions are not out of the woods. Despite the $47 billion and strong investment returns, the pension system still faces “a significant funding challenge,” per Reitmeyer. The funded ratio is only 56% (56 cents set aside for each dollar owed). The state will have to spend $7 billion+ a year for three decades before the pensions are fully funded. It would take until 2042 to reach the 80% funded-ratio to reinstate cost-of-living-adjustments (COLAs), but that would substantially increase pension liabilities, pushing the funded ratio down again. Do the math: that will require $100-$200 billion additional tax and lottery dollars, assuming no economic or market downturns. In the meantime, no retirees — neither current nor future — will have COLAs, so their pensions will continue to be eroded by inflation, and almost half of teachers will remain stuck in inadequate, Tier 5 pensions.

This is not a sustainable solution to New Jersey’s long-term debt problems. Murphy pumped $47 billion of good money after bad at the behest of his most powerful supporter, the NJEA. The money would have been better used to restructure the pension system and better align the state’s revenues with ALL its long-term liabilities. Unfortunately, it looks like Gov. Sherrill is going down the same path.

*According to the Government Accounting Standards Board (GASB), once New Jersey made a full payment in FY2022, it was then assumed that New Jersey would continue to make full payments until pensions were 100%-funded. This allowed the state to use a much higher discount rate based the assumed 7% rate for its investment returns. This caused the present value of pension liabilities to plummet.