NJ’s First Black Rhodes Scholar Speaks Out for Education Equity and Against Powerful Special Interests

January 19, 2021

NJ Economy Is Underperforming Again: 350,000 Fewer Jobs than Before Pandemic

January 25, 2021

We’re going to get a little wonkish here and delve into the mechanics of pensions because NJ’s public pensions are a disaster waiting to happen. At 38%, they are the worst funded public pensions in the nation. Absent a federal bailout, NJ is going to hit a budgetary wall in the relatively near future.

In a piece for Project Syndicate, Ben Meng, the former CIO of Calpers (CA’s largest public pension system) identifies the problems that confront pension systems like NJ’s and offers his solution. SUNLIGHT’S COMMENTS ARE IN ALL CAPS.

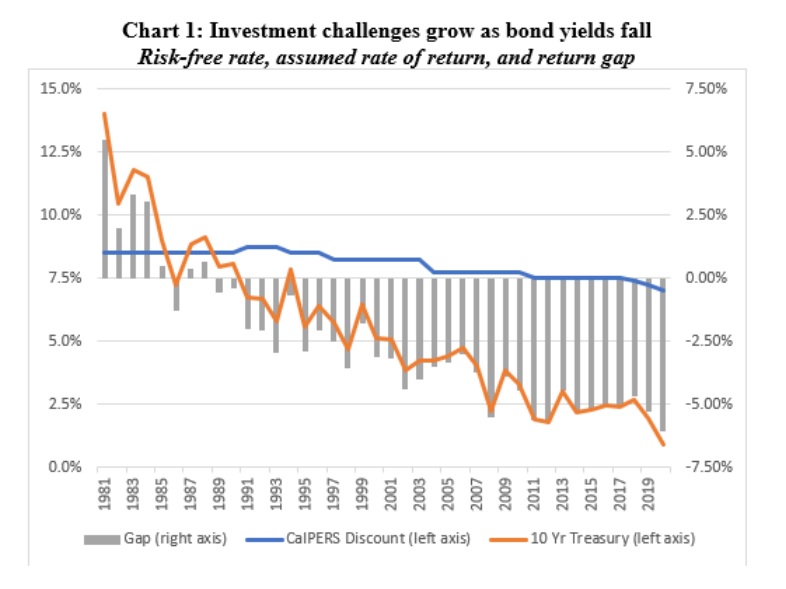

“The main challenge facing the public pension industry is the high assumed rates of returns on pension assets relative to what equities or bonds are likely to deliver.Many US public pension funds expect a rate of return in the neighborhood of 7% per year. But in today’s capital-market environment, achieving that sustainably over the long term has become an increasingly daunting task.

Today … the risk-free rate is more than six percentage points below targeted return.

Closing the gap will require innovation, new skills, and a greater appetite for risk. But investors today face a unique challenge in the form of the “triple low”: a low real interest rate, low inflation, and low economic growth. These conditions imply that future returns will likely lag well behind historical norms.”

THIS IS NEW JERSEY IN A NUTSHELL: NJ HAS A 7% ASSUMED RETURN, WHICH IS FAR ABOVE THE RISK-FREE RATE AS SHOWN IN THE GRAPH.

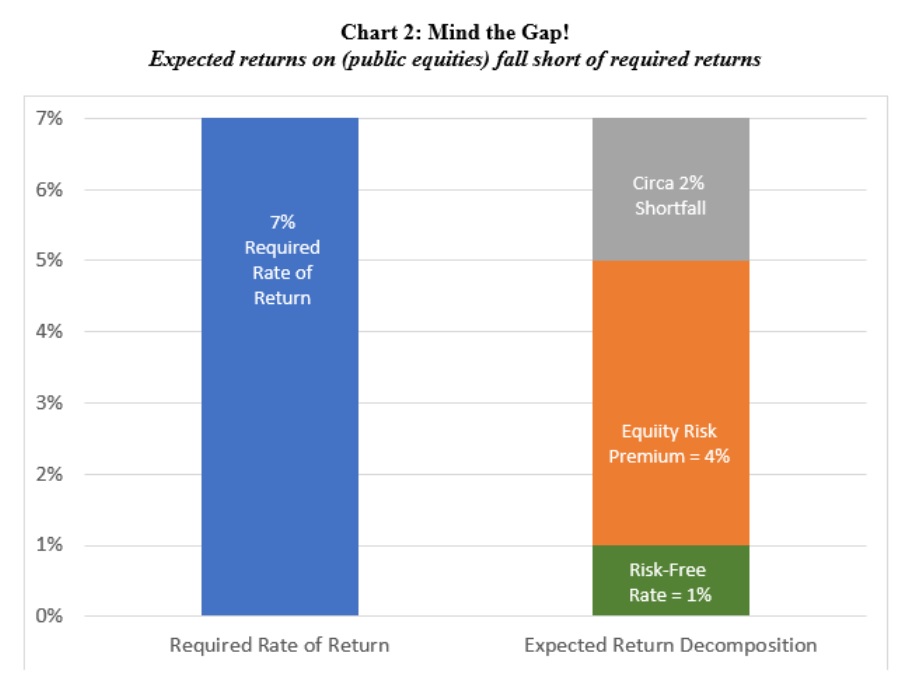

“Thus, as Chart 2 illustrates, the most that one can expect from a public-equity-only portfolio in the long run is a return of around 5% – well short of the 7% target.

IN OTHER WORDS, IT WILL BE VERY DIFFICULT FOR NJ TO MEET ITS 7% RETURN BOGEY, AND ANY SHORTFALL MEANS THAT UNFUNDED LIABILITIES WILL INCREASE AND THAT NJ TAXPAYERS WILL BE ON THE HOOK FOR ANY SHORTFALL.

“Because asset ownership reinforces one’s ability to pursue long-term investments, private equity – with its long tie-up periods – is an ideal asset class for public pensions. But building a suitable private-equity portfolio is no small matter. Knowing which private-equity managers to pick requires deep, specialized knowledge; and getting allocations from the best managers is often difficult. Moreover, private equity is not cheap. The top managers demand high fees, and their strategies often lack the transparency of public markets.”

BECAUSE OF THE NEED FOR HIGH RETURNS, MENG RECOMMENDS PRIVATE EQUITY, BUT PRIVATE EQUITY MANAGERS REQUIRE HIGH FEES. NJ HAS LONG BEEN A STATE WHERE POLITICIANS COMPLAIN ABOUT HIGH FEES. WILL GOV. MURPHY EVEN ALLOW FOR HIGH FEES? IS PRIVATE EQUITY EVEN AN OPTION FOR NJ?

“Beyond investing in “better” assets, public pensions can also try to close the gap between expected and target returns with “more” assets. By using moderate borrowing (leverage), pension funds can increase the volume of total assets under management and thereby boost overall returns.”

SUNLIGHT TAKES ISSUE WITH MENG’S IDEA OF MODERATE BORROWING TO JUICE RETURNS. IN ORDER TO BOOST RETURNS, NJ WILL CONTINUE TO INVEST IN RISKIER AND RISKIER ASSETS (AND AWAY FROM LOW-YIELDING, ULTRA-SAFE GOVERNMENT BONDS). PRIVATE EQUITY IS A RISKY ASSET. SO MENG IS ADVISING NJ TO INVEST IN RISKY ASSETS WITH BORROWED MONEY. THIS WOULD BE AKIN TO ISSUING MORE PENSION OBLIGATION BONDS (POBS), WHICH HAVE BEEN A DISASTER FOR NJ. IN FACT, THE LEGISLATURE HAS BANNED POBS. SUNLIGHT BELIEVES THAT BORROWING MONEY TO INVEST IN RISKY ASSETS IS A BAD IDEA FOR NJ.

SUNLIGHT’S MAIN POINT IS THAT NJ HAS DUG ITSELF A VERY DEEP HOLE, AND THAT MENG’S SOLUTION IS A VERY RISKY, ALMOST DESPERATE ONE. THE BETTER CHOICE WOULD BE TO REFORM NJ’S BROKEN PUBLIC PENSIONS.