As NJ Continues to Lose Wealth, It’s Premature to Judge the Full Impact of the SALT Cap

June 3, 2021

Fortune 500 Companies Are Fleeing NJ, and So Are Jobs and Wealth

June 9, 2021

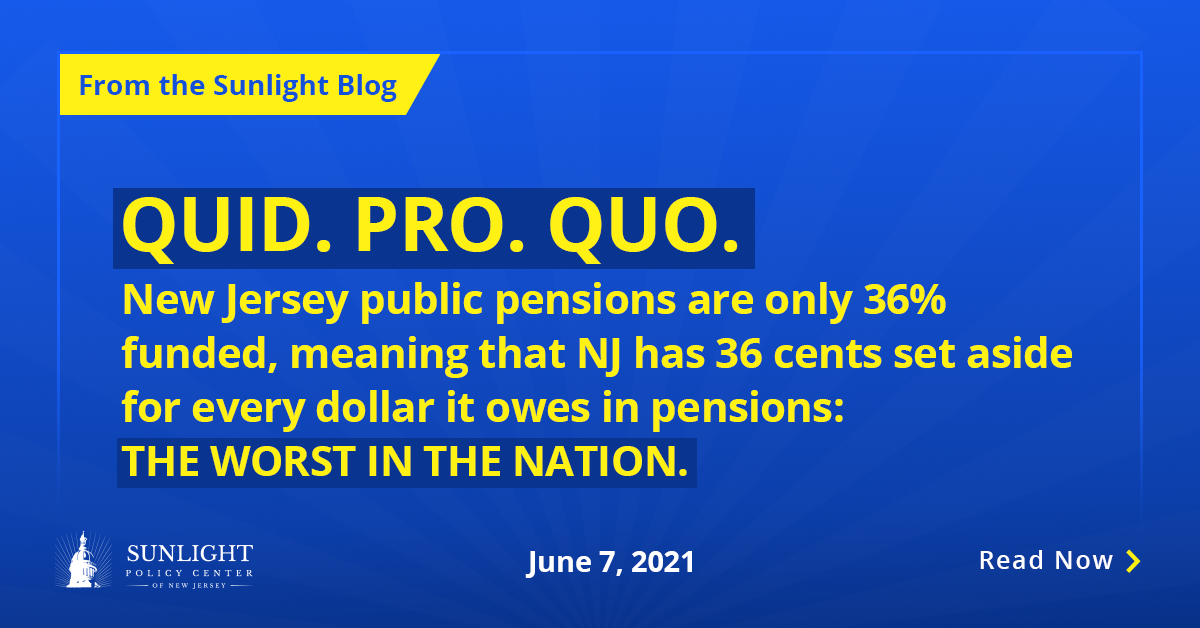

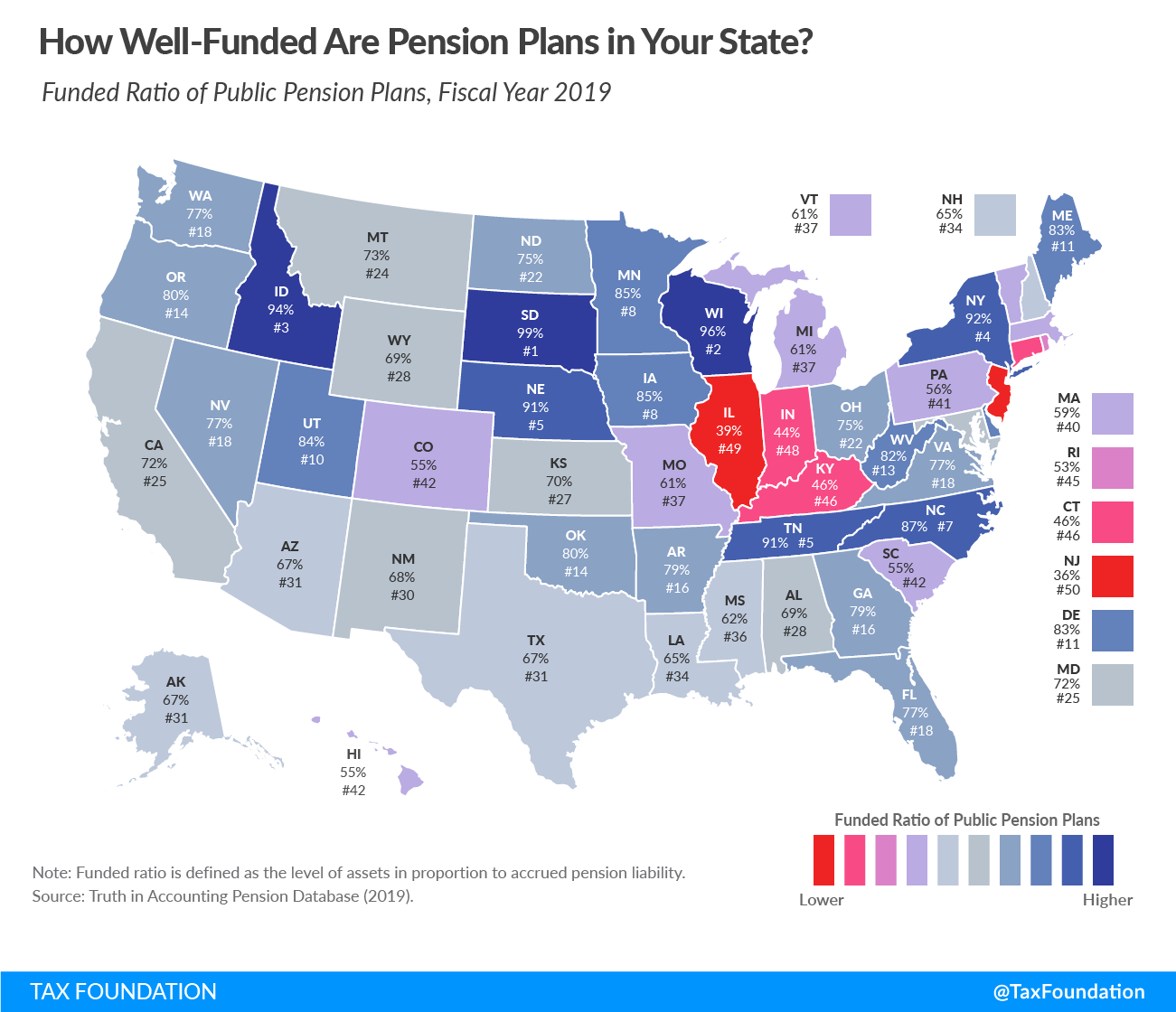

Just as Politico is reporting that Gov. Murphy is considering making a payment even larger than last year’s $6.4 billion (14% of the entire state budget) into NJ’s broken public pension system, the Tax Foundation came out with a report that underscored how Murphy is throwing billions of good money after bad. The report determined that as of June 2019 overall NJ public pensions were 36% funded, meaning that NJ has 36 cents set aside for every dollar it owes in pensions – THE WORST IN THE NATION – and worse even than broke Illinois, the only state with a lower debt rating than NJ.

{kind=link}

As highlighted by Sunlight for years, the report also showed that the Teachers Pension and Annuity Fund, NJ’s largest public pension fund, was only 27% funded. TPAF remains one of the single worst public pension funds in the nation. As of June 2020, TPAF was 24.6% funded. TPAF has had stellar returns since then, but because the asset level is so low, even better returns will not save an unreformed TPAF, which the Brookings Institute has projected will run out of money in 12-15 years.

Murphy’s billions in pension payments please his NJEA patrons because they help obscure the fact that the NJEA, itself, bears responsibility for the severe underfunding of TPAF. But dumping $6.4-plus billion into a broken and unreformed TPAF ill-serves NJ citizens because these billions should be used to shore up a restructured and sustainable TPAF. Both teachers and the state would benefit.

But rather than do the right thing by both NJ teachers and NJ citizens, Murphy chooses to please his special interest pals. After all, 2021 is an election year and Murphy will get millions in NJEA support.

Quid. Pro. Quo.

NOTE ABOUT FUNDED LEVELS: The Tax Foundation’s funding levels are drawn from state’s own 2019 pension reports based on the Government Accounting Standards Board (GASB) methodology. GASB uses more conservative discount rates because of the very large amount of unfunded liabilities, which are not backed by assets and therefore should not use asset return assumptions as the discount rate. The GASB numbers stand in sharp contrast to the state’s own methodology, which uses an unrealistically high discount rate to arrive at much rosier but misleading funded levels, which are often reported in the media.